Fillable Form Promissory Note

Promissory Note contains a written promise of a party to pay another party on a specified future date.

What is a Promissory Note?

A promissory note is a written promise by one party to another, usually in the form of an enforceable legal document, to pay a certain amount of money at a specified date or on demand. The promissory note outlines the terms and conditions for payment, including the amount owed, interest rate if applicable, date of payment, and the parties involved. It is important to note that a promissory note can be used as collateral in order to secure a loan or other credit agreement, and is often referred to as an IOU (I owe you).

What are the types of promissory notes?

There are many different types of promissory notes with varying degrees of formality. Here is an overview of some common types:

Simple Promissory Note:

Secured Promissory Note:

Demand Promissory Note:

Revolving Promissory Note:

Negotiable Promissory Note:

A simple promissory note is a written agreement between two parties that outlines the terms of a loan, including the repayment amount, payment due date, and interest rate (if applicable). This type of note does not require collateral or any additional paperwork beyond what is outlined in the promissory note itself.

A secured promissory note is a written agreement between two parties that outlines the terms of a loan, including the repayment amount, payment due date, and interest rate (if applicable). This type of note requires collateral from one party in order to secure the loan or credit agreement. The most common type of collateral used in secured promissory notes is property or other valuables.

A demand promissory note is a written agreement between two parties that outlines the terms of payment, including the amount owed, interest rate (if applicable), and date of payment. This type of note requires payment upon demand, meaning that the lender can demand payment at any time without any notice.

A revolving promissory note is a written agreement between two parties that outlines the terms of a loan, including the repayment amount and interest rate (if applicable). This type of note allows for multiple payments to be repaid over a certain period of time, with each payment reducing the remaining balance due.

A negotiable promissory note is a written agreement between two parties that outlines the terms of a loan, including the repayment amount and interest rate (if applicable). This type of note can be transferred or sold to another party, allowing the note holder to receive a sum of money in exchange for their promissory note.

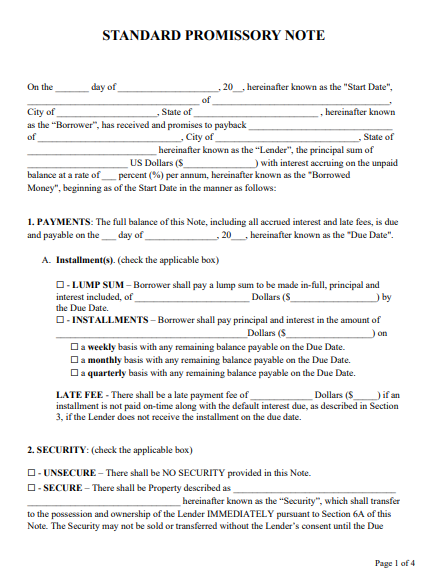

What are the parts of a Promissory Note?

A promissory note is a binding document between borrower and lender that establishes the terms of a loan, so it's important that all conditions are explicitly clear from the start. Below are eight parts that can be typically found in a legally binding promissory note:

Principal debt: The owed amount that the borrower has agreed to pay back to the lender over a set period of time is called the principal debt.

Date of issuance: The date of issuance on a promissory note is the day and time that the loan begins. This also starts the period during which repayment is due.

Maturity date: The maturity date is the final day indicated on a promissory note by which the borrower must pay back the entirety of the loan.

Repayment schedule: The repayment schedule the borrower must follow is generally laid out in the promissory note. For example, some loans may be paid incrementally through monthly payments, while others require a lump sum at the maturity date.

Interest rate: A promissory note typically includes the amount of interest that a borrower will agree to pay the lender as a fee for granting them the loan. Interest may be charged incrementally, fixed-rate percentage of the unpaid balance of the loan, or variable rate changing with time.

Amount to be repaid: A promissory note may also state the total amount owed by the borrower, which is comprised of both the initial loan amount and any interest collected up to that point.

Collateral: In the event that the borrower defaults on the loan, any property or possessions listed as collateral by the lender may be used to secure repayment. This gives the lender peace of mind in issuing the loan.

Signatures: The final step to creating a promissory note is to have both parties sign the document and make sure that it is properly dated. Once this is done, the agreement between the two parties involved will be legally binding and enforceable in court.

What are the advantages and disadvantages of a promissory note?

Advantages: Promissory notes generally provide more security to lenders than other types of credit agreements because they are legally binding and enforceable documents. Promissory notes also offer flexibility for both parties as the terms and conditions can be tailored to meet specific needs. Additionally, interest rates may be lower than those offered on other types of loans, making them attractive for borrowers.

Disadvantages: Promissory notes are subject to certain risks such as default or bankruptcy, which could result in a loss for the lender. Additionally, since promissory notes are considered a form of secured debt, the lender may be able to repossess the collateral in case of default. Finally, borrowers should keep in mind that if they default on their loan or fail to make payments as agreed upon, this could have an adverse impact on their credit score.

Who can issue a promissory note?

A promissory note can be issued by any person or group of people, including individuals, businesses, corporations, or government entities. The party issuing the note is referred to as the “maker” and is responsible for repaying the debt according to the terms and conditions outlined in the document.

What is the validity period of a promissory note?

The validity period of a promissory note can vary depending on the terms and conditions outlined in the document. Generally, promissory notes are valid for a set amount of time that is specified by both parties in the agreement. It is important to ensure that all payments are made before the end date listed in the note in order to avoid defaulting on the loan. Additionally, it is important to understand that some promissory notes may be renewed or extended upon agreement of both parties. It is important to review the terms and conditions carefully before entering into any type of agreement involving a promissory note.

It is also important to keep in mind that if a promissory note is not paid off within the specified time frame, then it may be subject to legal action or collection efforts. It is important to make sure that all payments are made on time and in full according to the terms outlined in the promissory note. If a borrower defaults on the loan, this could have an adverse effect on their credit score as well. Borrowers should always make sure that they understand the terms and conditions outlined in the promissory note before entering into any type of loan agreement. Finally, borrowers should keep records of all payments made in order to ensure that their payments are accounted for correctly.

By understanding the different aspects of a promissory note, borrowers can ensure that they make informed decisions when entering into any type of loan agreement. With the right information and guidance, borrowers can protect their finances and credit scores by making sure that all payments are made on time according to the terms and conditions outlined in the promissory note. By taking these steps, borrowers can help avoid any potential legal action or collection efforts regarding their promissory note.

How to write a promissory note?

Define the Terms and Conditions of the Promissory Note: Before initiating a promissory note, the borrower and lender must first agree on the terms of the loan. This should include information such as the amount being borrowed, repayment period, interest rate, fees, late payment fees, payment schedule, and any other applicable clauses.

Draft the Promissory Note Agreement: The next step is to draft the promissory note agreement. This should include all of the agreed upon terms and conditions of the loan, including any applicable clauses or special provisions. Additionally, it should also include contact information for both parties, as well as a signature line where each party can sign off on the agreement.

Have the Promissory Note Notarized: In order for the promissory note to be legally binding, both parties must have it notarized by a qualified notary. This will help protect each party's interests in case there is an issue with repayment or any other aspect of the loan agreement.

File the Promissory Note: After the promissory note is notarized, both parties should make sure to file it with their local courthouse or other appropriate government agency in order to ensure that it is legally binding and enforceable.

Keep Records of All Payments: It is also important for both parties to keep accurate records of all payments made on the loan. This will help ensure that there are no issues with repayment or any other aspect of the promissory note. Additionally, this can also help protect both parties in case of any legal disputes regarding the agreement.

What happens if a promissory note is not paid?

If a borrower defaults on their promissory note, they may be subject to legal action or collection efforts. This could have an adverse effect on the borrower’s credit score and can potentially lead to additional financial problems. Additionally, if the lender is unable to recover the full amount owed from the borrower, then they may choose to pursue legal action to reclaim the remaining balance. It is important for borrowers to make sure that they understand all of the terms and conditions outlined in their promissory note before entering into any type of loan agreement. Additionally, borrowers should always keep accurate records of all payments made on the loan in order to ensure that their payments are accounted for correctly.

Does a promissory note need to be notarized?

Yes, a promissory note must be notarized in order to be legally binding. Notarizing the document will help protect both parties in case of any legal disputes regarding the loan agreement. Additionally, it is important for both parties to make sure that they file the promissory note with their local courthouse or other appropriate government agency in order to ensure that it is legally binding and enforceable.

What voids a promissory note?

A promissory note can be voided if either party has entered into it under false pretenses or with fraudulent intent. Additionally, if the borrower is unable to keep up with payments, then this could potentially void the promissory note as well. It is important for both parties to make sure that they understand all of the terms and conditions outlined in the promissory note before entering into an agreement. Additionally, both parties should make sure that they keep accurate records of all payments made on the loan in order to ensure that their payments are accounted for correctly.

What happens if a promissory note is not honored?

If a promissory note is not honored, then the lender may pursue legal action in order to reclaim the balance that is owed. This could have an adverse effect on the borrower’s credit score and can potentially lead to additional financial problems. Additionally, if the lender is unable to recover the full amount owed from the borrower, then they may choose to pursue legal action to reclaim the remaining balance. It is important for both parties to make sure that they understand all of the terms and conditions outlined in their promissory note before entering into any type of loan agreement. Additionally, borrowers should always keep accurate records of all payments made on the loan in order to ensure that their payments are accounted for correctly.