Fillable Form Direct Deposit Authorization

The Direct Deposit Authorization Form allows individuals to authorize the transfer of funds directly into their designated bank account. The form requires personal information, including bank account details and signature.

What is a Direct Deposit Authorization?

A Direct Deposit Authorization is a document used to authorize the transfer of funds directly into a designated bank account. This may be for payroll purposes, or other kinds of recurring payments. A Direct Deposit refers to the deposit of funds electronically into a bank account rather than through a physical, paper check.

The form requires personal and financial information, such as a person’s full legal name and bank account details. This information is necessary in order to ensure that the correct payment is the correct account. The form must also be signed by the person providing authorization in order to certify that they understand and agree to share this information for the purpose of a direct deposit.

Because the form contains such sensitive information about a person’s bank account and their signature, it is very important that a Direct Deposit Authorization be kept in a safe and secure place so as to avoid problems like fraud or the transaction not being properly executed.

How do I fill out a Direct Deposit Authorization?

Direct Deposit Authorizations require information such as your full legal name and your bank account details. Make sure that all information entered is correct and true in order to avoid any legal issues.

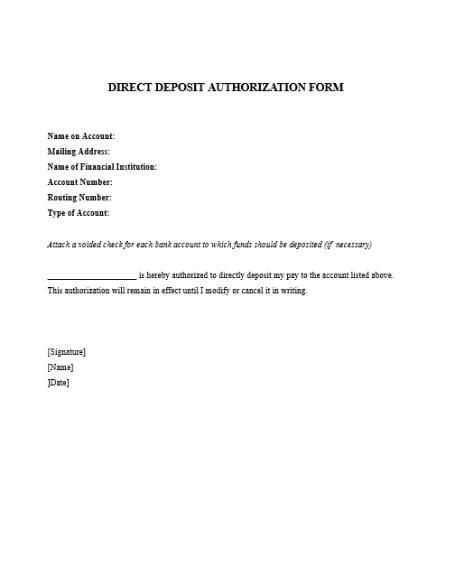

Step 1: Name on Account

Enter the name associated with the bank account that the funds will be deposited to.

Step 2: Mailing Address

Enter the mailing address of the account holder.

Step 3: Name of Financial Institution

Enter the name of the financial institution (such as a bank) that the account holder is using.

Step 4: Account Number

Enter the account number associated with the recipient’s bank account.

Step 5: Routing Number

Enter the routing number associated with the bank.

Step 6: Type of Account

Enter the type of account that the payment is being deposited to (i.e. a current account, savings account, salary account, or other).

Step 7: Authorization

Enter a short message in the space provided authorizing that the payment be directly deposited to the account whose details are listed above. Enter the depositor’s full legal name. More terms and conditions may be added here, should they be necessary and all parties agree to them.

Step 8: Name and Signature

Have the recipient of the funds (the owner of the above bank account) write their full legal name and sign the form in the spaces provided.

Frequently Asked Questions (FAQs)

What is a routing number?

A routing number is a nine-digit bank identification number that serves as a numerical address that allows a bank to send and receive money from other financial institutions. The routing number identifies the financial institution responsible for the payment and ensures that funds go to the right place.

Where can I find my routing number?

The routing number can be found around the bottom left corner of a check, on your banking statement, through your bank’s online portal, or by contacting your bank directly.

What are the pros of direct deposits?

Transactions made through direct deposit are generally easier to track than physical transactions while also being more convenient, as the transaction happens entirely online.

How do banks manage direct deposit payments?

Banks use a system called the Automated Clearing House (ACH) to facilitate financial transactions that occur online.

How safe is a direct deposit transaction?

Direct deposits are regulated and protected under the Electronic Funds Transfer Act (EFTA). The EFTA outlines requirements for banking institutions and consumers to follow when errors occur, which allows customers to challenge errors, have them corrected, and receive limited financial penalties.

Are direct deposit transactions safer than checks?

Yes. If a check is lost, a person’s bank information is put at risk due to the account number and routing number being written on the check. Because direct deposits do not rely on physical paper checks, and funds transferred are protected by the EFTA, there is much less risk involved in paying for things through direct deposits.

What are the cons of direct deposits?

As with all online processes, direct deposits are vulnerable to possible cybercrimes like hacking and information leaking. However, all financial institutions are well-acquainted with the dangers of cybercrimes, and so are always improving existing cybersecurity measures and implementing new ones. Direct deposits also require both parties involved to have a bank account, which is not always something that a person has.

Do direct deposits require the depositor’s information?

Aside from their name, no. This is intentional so as to minimize the risk to the depositor’s own financial information. As much as possible, only information that is necessary for the transaction should be included in a Direct Deposit Authorization or any other kind of document concerning a transaction.

Can I enter someone else’s account in a Direct Deposit Authorization instead of my own?

Yes, but keep in mind that this means that the payment will be sent to their account and not yours. This will also require said person’s consent (preferably written), as it will also involve sharing their bank account information. The depositor must also be made aware of whose account information is being provided, and the reason for why the payment should be sent to their account instead.

How long does it take for bank accounts to reflect or receive a direct deposit payment?

Usually, payments made through direct deposit are received by the account immediately, barring any issues with the bank, the ACH system, or any other situation that may affect the bank’s ability to process payments.

Can direct deposit payments be made internationally?

Yes. However, take note that requires all direct deposit payments that are sent outside the U.S. to be identified and sent as International ACH Transactions (IATs) per the National Automated Clearing House Association (NACHA).

What happens if the direct deposit payment is rejected?

The balance should be returned to the payer’s account automatically. If the balance takes too long to be returned or is not returned, contact the depositor and your bank to work on resolving the issue.

What kinds of payments can direct deposits be used for?

Direct deposits are most commonly used for regular payments, such as paychecks and rent.

Can direct deposit payments be scheduled?

Yes. Any arrangements that require regular direct deposit payments will generally need to be outlined in the Direct Deposit Authorization and/or discussed with the bank that the transactions will be done through.

Can direct deposits be paid in advance?

Yes. This is called an Early Direct Deposit, and is usually applied to paychecks. It allows a person to access their paycheck earlier than the usual date. However, not all banks offer this service, so make sure to ask your employer and/or the bank for more details.

What should I do if there is an issue with the direct deposit?

Depending on what the issue is, the solution may be as simple as asking the depositor to review the transaction. To address more complex or major problems, the bank may need to be contacted in order to have them look into the issue.

What if a direct deposit happens without my consent?

If you find that money was subtracted from your account without your knowing, or that you received money from a suspicious source, it is vital that you call your bank immediately to report any such incidents, as they present a possible threat to your bank account.