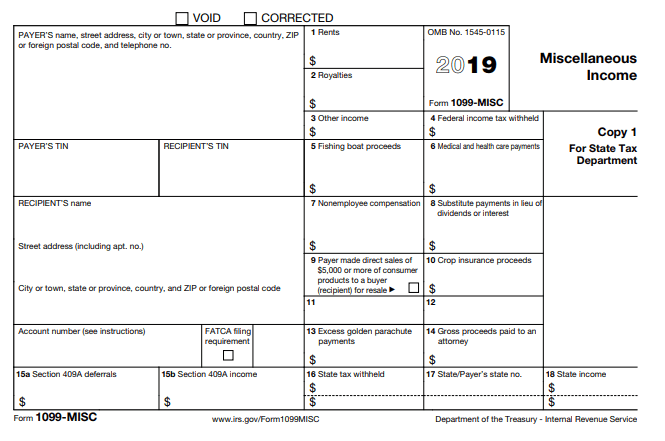

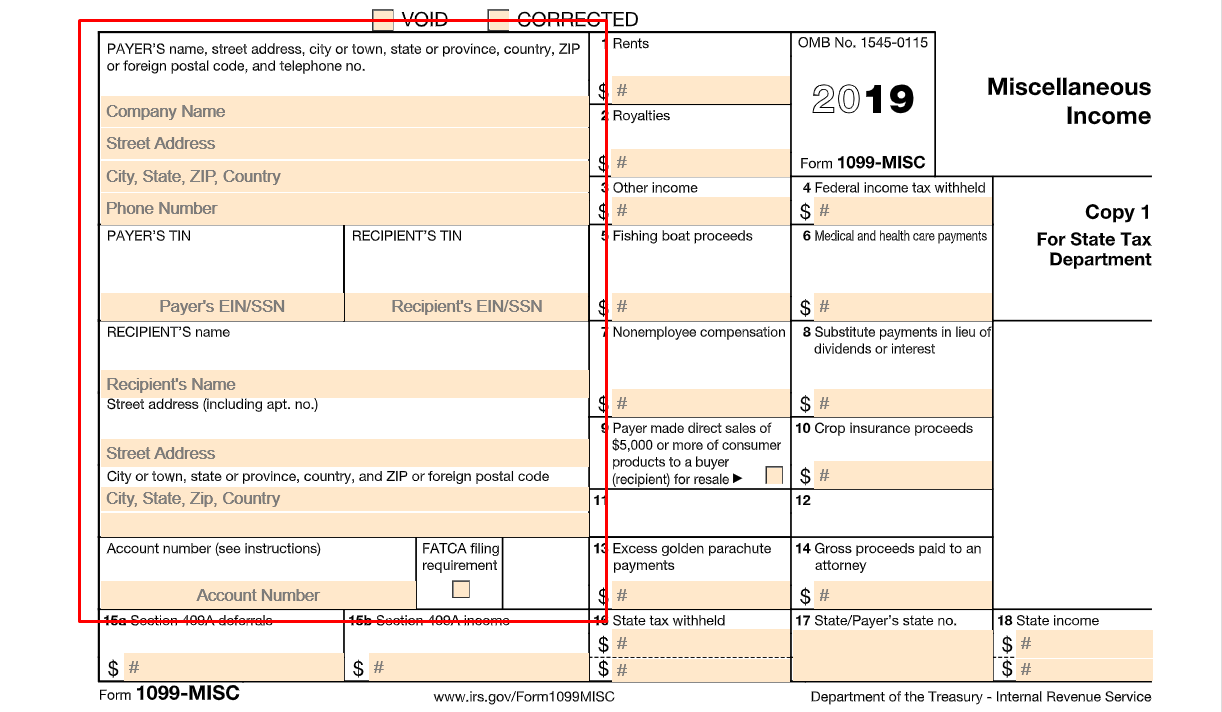

Fillable Form 1099 MISC

The 1099 MISC Form is used to report miscellaneous income to the IRS. They are used when you have paid a non-employee a total of at least $600 during the tax year.

What is Form 1099-MISC?

Officially Miscellaneous Income, Form 1099-MISC is an Internal Revenue Service (IRS) document that employers complete and file to report nonemployee compensations paid. It is a variant of Form 1099. According to the federal tax agency, filing Form 1099-MISC is mandatory. It serves a similar purpose to an independent contractor, self-employed individuals, freelancers, and sole proprietors as Form W-2 does to an employee.

Form 1099-MISC reports the amounts of non-employee compensations received by an individual during the year that he or she provided service. Businesses need to file the form for each person to whom they have paid one or more of the following:

- rents;

- services performed by someone who is not their employee;

- prizes and awards;

- other income payments;

- medical and health care payments;

- cash payments for fish (or other aquatic life) you purchase from anyone engaged in the trade or business of catching fish;

- generally, the cash paid from a notional principal contract to an individual, partnership, or estate;

- payments to an attorney; and

- any fishing boat proceeds.

Companies can file Form 1099-MISC by mail or online. If you are filing more than 250 information returns for a year, the federal tax agency requires that you file electronically.

Form 1099-MISC contains several copies and each copy has a different purpose.

How to Fill Out Form 1099-MISC?

Complete Form 1099-MISC by providing all the information it requests.

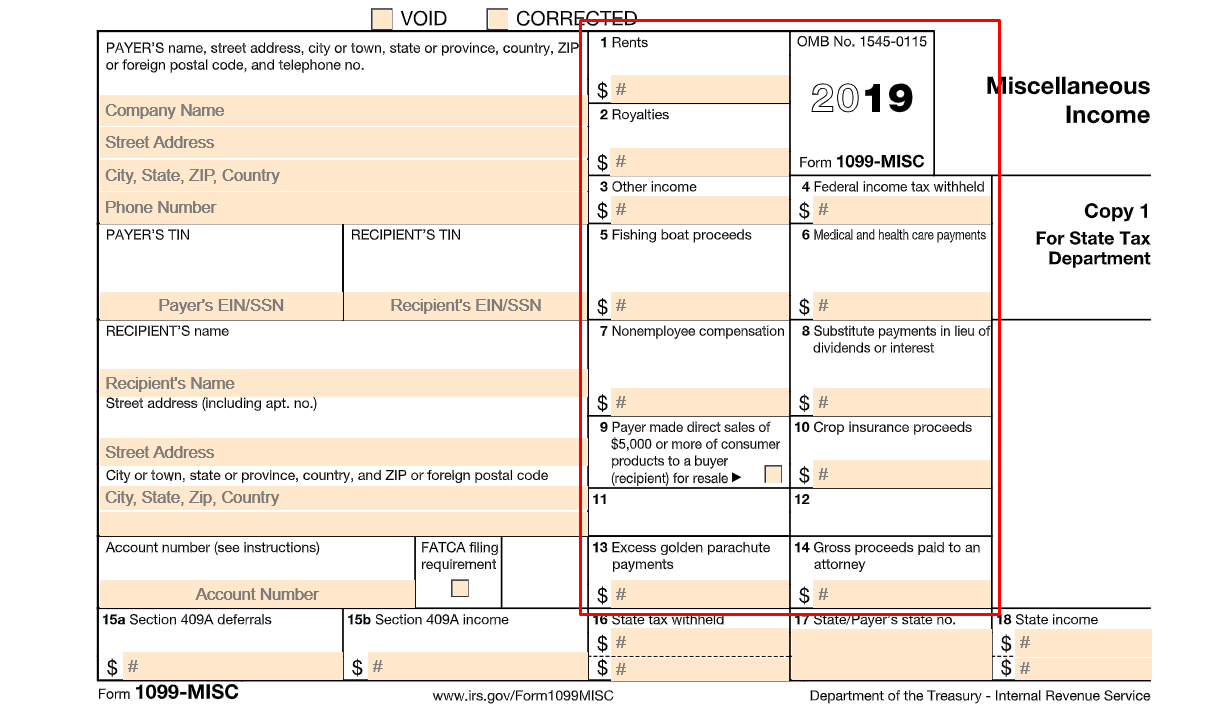

For the numbered boxes, provide the total amount paid in the boxes that apply. Leave the irrelevant boxes blank.

- 1 Rents asks for the total amount paid in rents.

- 2 Royalties asks for the total amount paid in royalties of any kind.

- 3 Other income asks for any payments made that do not fall under any of the categories provided.

- 4 Federal income tax withheld asks for the total amount of withheld federal income tax.

- 5 Fishing boat proceeds asks for the total amount paid to a crew member.

- 6 Medical and healthcare payments asks for the total amount paid to a health or medical professional.

- 7 Nonemployee compensation asks for the total amount paid to a hired nonemployee contractor.

- 8 Substitute payments in lieu of dividends or interest asks for “aggregate payments of at least $10 of substitute payments received by a broker for a customer in lieu of dividends or tax-exempt interest as a result of a loan of a customer’s securities.”

- 9 Payer made direct sales of $5,000 or more of consumer products to a buyer (recipient) for resale is a checkbox. Check it if you sold consumer products to an individual for resale that amounted to $5,000 or more.

- 10 Crop Insurance proceeds asks for the insurance proceeds paid to farmers.

- 11 Leave this blank.

- 12 Leave this blank.

- 13 Excess golden parachute payments asks for the total compensation of any excess golden parachute payments.

- 14 Gross proceeds paid to an attorney asks for the total amount paid to an attorney in connection with legal services.

- 15a and 15b Section 409A deferrals and income refer to Section 409A of the Internal Revenue Code. In 15a provide the deferred amount to be paid in a future year. In 15b, provide the income amount.

- 16 State tax withheld asks for the amount withheld for the contractor’s state taxes.

- 17 State / Payer’s state no. asks for payer’s state in abbreviated form and his or her state identification number.

- 18 State income asks for the amount of state payment.